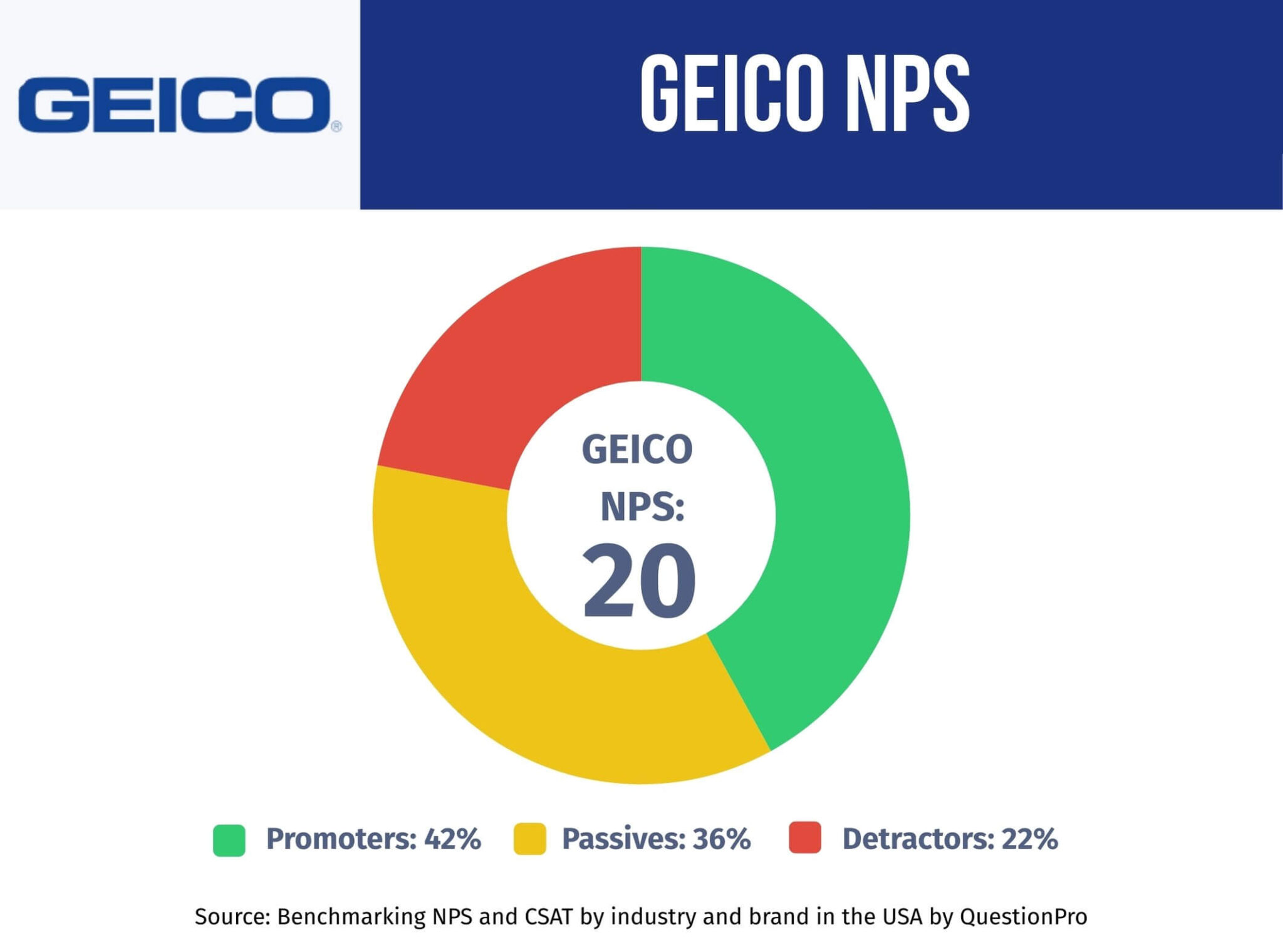

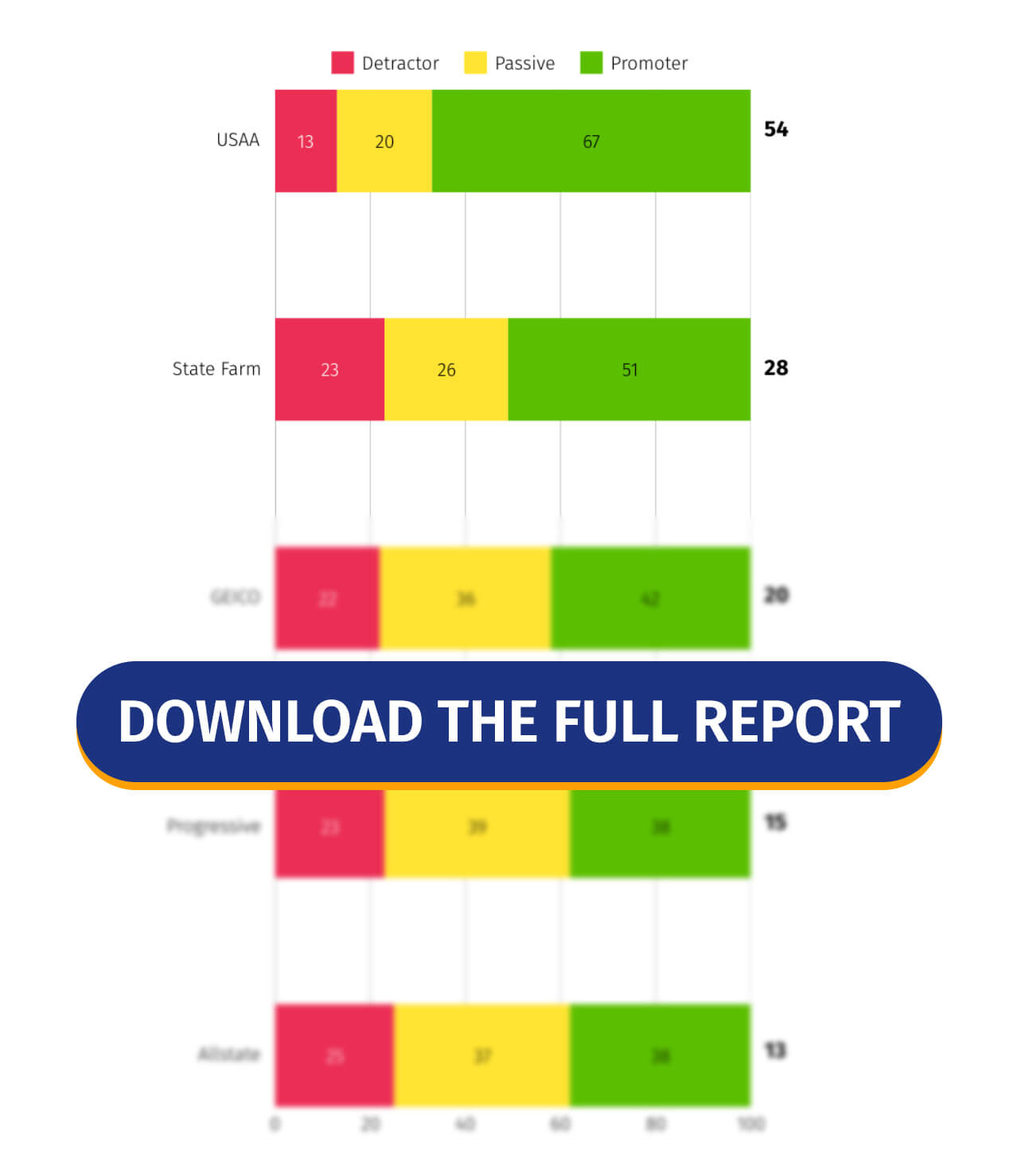

GEICO NPS is 20 in QuestionPro’s Q1 2025 Benchmarking NPS and CSAT Report. That places GEICO slightly below the insurance industry average of 23 and shows a clear loyalty gap for one of the most recognized insurance brands in the USA.

The score does not mean GEICO has a weak customer base. It means the company has a meaningful group of satisfied policyholders, but also enough neutral and dissatisfied customers to limit stronger brand advocacy.

For insurance companies, NPS matters because loyalty is tested during moments that customers remember most: filing a claim, asking about a rate increase, changing a policy, speaking with support, or trying to understand coverage.

What is Net Promoter Score?

Net Promoter Score, or NPS, measures how likely customers are to recommend a company, product, or service to someone else.

A standard Net Promoter Score survey asks customers to answer one question on a 0 to 10 scale: “How likely are you to recommend this company to a friend or colleague?” QuestionPro explains that NPS responses are used to create a score from -100 to +100 and act as an indicator of customer experience, loyalty, satisfaction, and brand loyalty.

Customers are grouped into three categories:

- Promoters: Customers who score 9 or 10. They are loyal, satisfied, and more likely to recommend the brand.

- Passives: Customers who score 7 or 8. They are satisfied but not strongly loyal.

- Detractors: Customers who score 0 to 6. They are unhappy or frustrated and may share negative feedback.

The formula is simple:

NPS = % Promoters – % Detractors

For GEICO, the result is 20 because 42% of respondents are promoters and 22% are detractors.

What Is GEICO’s NPS Score in 2025?

GEICO’s NPS score in 2025 is 20, based on QuestionPro’s Q1 2025 Benchmarking NPS and CSAT Report

The customer response breakdown is:

| Customer group | Score range | GEICO result |

|---|---|---|

| Promoters | 9 to 10 | 42% |

| Passives | 7 to 8 | 36% |

| Detractors | 0 to 6 | 22% |

The NPS calculation is:

42% Promoters – 22% Detractors = NPS 20

This means GEICO has more promoters than detractors, which is positive. But the 36% passive group is important. These customers may be satisfied enough to stay for now, but they are not loyal enough to strongly recommend GEICO to others.

How Does GEICO Compare to the Insurance Industry Average?

GEICO’s NPS score of 20 is slightly below the insurance industry average of 23 in QuestionPro’s Q1 2025 Benchmarking NPS and CSAT Report.

That gap is not huge, but it is worth paying attention to. Insurance is a competitive category, and many customers compare providers based on price, claims experience, service quality, and trust. A three-point gap can signal that GEICO is close to the industry average but not leading on customer loyalty.

The benchmark also gives GEICO a clear target. To move above the industry average, the company would need to reduce detractors, convert more passives into promoters, or do both.

What Does GEICO’s Customer Breakdown Show?

GEICO’s customer breakdown shows that the brand has a strong base of promoters, but the passive group may be holding the score back.

The 42% promoter share suggests many policyholders have had a good enough experience to recommend GEICO. This may reflect competitive pricing, brand familiarity, digital convenience, or positive service interactions.

The 36% passive share is the biggest opportunity. Passive customers are not necessarily unhappy. They may simply feel the experience is average, transactional, or easy to replace. In insurance, passives can switch quickly when another provider offers a lower rate or a smoother claims experience.

The 22% detractor share is the main risk area. Detractors are more likely to leave, complain, or discourage others from choosing the brand. For insurance companies, detractors often come from moments of friction, especially around claims, billing, policy changes, and support.

What May Be Affecting GEICO’s NPS?

Several customer experience factors may be affecting GEICO’s NPS. These themes should be treated as experience signals, not as universal claims about every policyholder.

Customer service and communication

Policyholders often judge insurance companies by how easy it is to reach support and get a clear answer. Long wait times, repeated transfers, unclear updates, or difficulty reaching a person can create frustration.

For GEICO, improving communication around billing, policy changes, and claims status could help reduce customer effort and build more trust.

Rate increases and pricing perception

Insurance customers are sensitive to premium changes, especially when they do not understand why rates increased. Even when pricing changes are driven by broader market conditions, customers may still feel surprised or treated unfairly.

A clearer explanation of rate changes could help reduce dissatisfaction among long-term policyholders.

Claims handling

Claims are one of the most important insurance touchpoints. A customer may tolerate small service issues during normal policy management, but a poor claims experience can quickly turn into a loyalty problem.

Delays, unclear next steps, limited updates, or disagreement over payout decisions can affect how customers rate the brand.

Policy transparency

Insurance policies can feel confusing. Customers want to know what is covered, what is excluded, and what happens when they need help.

When customers feel surprised by policy rules or unclear fees, trust can drop. Clearer policy communication can help prevent frustration before it becomes a detractor response.

Loyalty experience

Long-term customers often expect their history with a provider to matter. If they feel treated the same as a new customer during a problem, they may question the value of staying.

For GEICO, improving the experience for long-term policyholders could help move more customers from passive to promoter.

How Can Insurance Companies Improve NPS?

Insurance companies can improve NPS by focusing on the parts of the customer journey that create the strongest emotional response. In insurance, those moments usually include claims, billing, renewals, rate changes, and customer support.

Useful steps include:

- Ask the NPS question after key touchpoints, not only once a year.

- Add an open-ended follow-up question to understand the reason behind each score.

- Segment results by claim type, policy type, region, and customer tenure.

- Follow up with detractors quickly when the issue is fixable.

- Study passive customers to find what stops them from becoming promoters.

- Compare NPS with CSAT, customer effort, complaints, and retention data.

- Track improvement over time instead of treating NPS as a one-time score.

Insurance teams can also compare NPS with complaint data. For example, the NAIC Complaint Index is often used to compare insurance complaints relative to company size and market share, which can give additional context alongside customer loyalty scores.

How Can QuestionPro Help Measure Insurance NPS?

QuestionPro helps companies measure NPS by collecting customer ratings, grouping customers into promoters, passives, and detractors, and capturing the reason behind each score.

For insurance teams, this can be useful after claims, renewals, customer service calls, policy updates, or billing interactions. QuestionPro’s NPS tools include the standard 0 to 10 NPS question and AskWhy, which combines NPS with root-cause feedback and comments.

A customer experience management platform can also help teams connect feedback with dashboards, journey insights, and closed-loop workflows. QuestionPro Customer Experience supports customer feedback, journey management, CX dashboards, and closed-loop action, which are useful when teams need to turn NPS feedback into practical improvements.

Stay Ahead with the Latest NPS Insights

GEICO’s NPS score of 20 shows that the brand has a positive loyalty position, but it is not ahead of the insurance industry benchmark. With an insurance average of 23, GEICO sits close to the category but still has room to improve.

The biggest opportunity is the passive group. These customers are not fully dissatisfied, but they may not feel enough trust, value, or service confidence to recommend GEICO. Improving claims communication, pricing transparency, policy clarity, and support experiences could help turn more passive customers into promoters.

For any insurance company, NPS is most useful when it leads to action. The score shows where loyalty stands. The follow-up feedback explains what needs to change.

Download the Q1 2025 NPS Benchmark Report and uncover how industry leaders are building strong customer loyalty through exceptional experiences.

Looking to elevate your Net Promoter Score? Contact the experts at QuestionPro for personalized strategies and tools to measure, track, and improve customer satisfaction at every touchpoint.